By Anirudh Shingal

The European Union and India launched negotiations towards a free trade agreement (a “FTA”) in June 2007. After several rounds, these negotiations entered an intense phase following the February 2012 EU-India Summit. Both partners would like the negotiations to conclude by the next summit. One of the important issues in this agreement, officially called the Bilateral Trade and Investment Agreement (the “BTIA”), is the overall ambition of the services package.

The services sector is extremely important for the EU and India in the on-going trade negotiations. Both the EU and India are predominantly service economies with more than 70% and 50% of their respective GDPs emanating from services. Thus, any trade agreement between the two that excludes services would ipso facto exclude the most important sectors for both partners. Moreover, there are significant barriers to services trade between the two, so that substantial coverage of services in a likely agreement could help to deliver improved access to both markets and also lead to more rapid liberalization of India’s services than can arguably be accomplished unilaterally. While services liberalisation offers direct benefits, much like goods liberalisation, the research literature suggests the presence of more comprehensive systemic benefits via the positive impact of services liberalization on manufacturing productivity. See, e.g., Arnold et. al, 2006a, b, 2007. Thus, the benefits to both economies from services liberalization will almost certainly be larger than those from goods trade liberalisation.

Stylized Facts

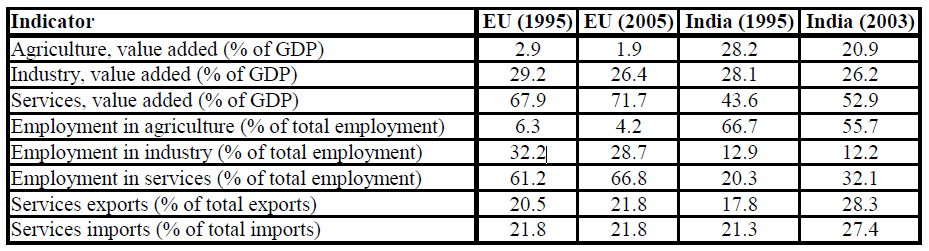

The services sector accounts for more than half of India’s GDP and its importance as an employer has been growing over time, rising from 20% of total employment in 1995 to one-third of the total at present. For the EU as well, the sector contributes more than 70% of GDP and two-thirds of total employment. The same holds true of trade in services, which has also witnessed rapid growth in both economies. Services trade accounts for a fifth of all trade for the EU, while for India this share is even higher. See Table 1, taken from a study done for the Commonwealth Secretariat (2009), summarises these data. The table demonstrates the importance of the services sector from the perspective of the BTIA between the EU and India.

Table 1: Summary Data on the Significance of Services

Source: Commonwealth Secretariat, Innocent Bystanders: Implications of an EU-India Free-Trade Agreement for Excluded Countries, Commonwealth Secretariat, London (Feb, 2009).

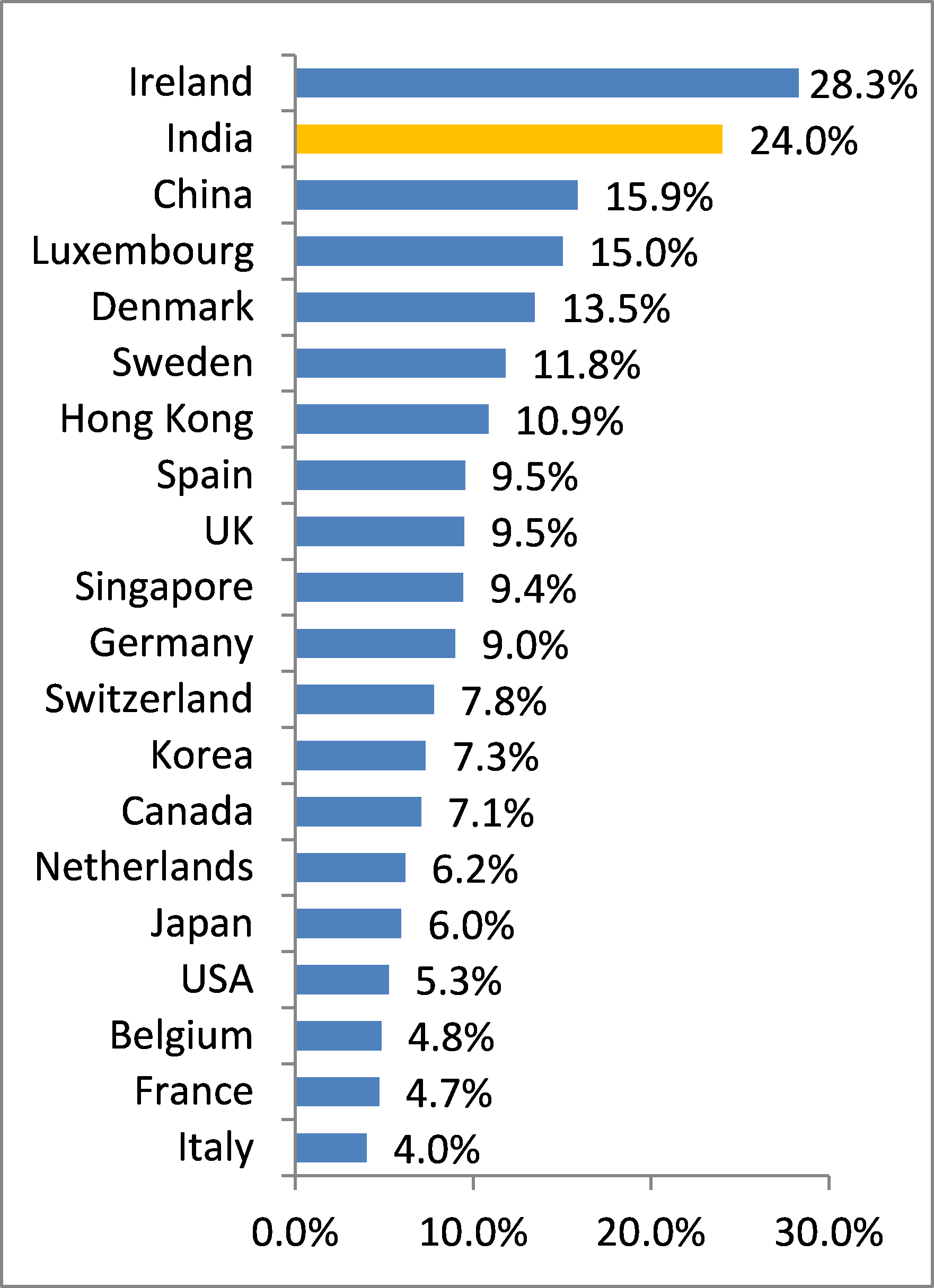

Examining services trade more closely, India witnessed the second fastest growth in services trade over 1996-2006 amongst the top twenty services traders in 2006, with a growth rate of 24% per annum for services exports and 17.4% per annum for services imports (see Figure 1 below). With the exception of Ireland, which tops the list in both cases, India’s growth rate, especially of services exports, is considerably higher than that of other EU Member States as well as the rest of the “Quad” (US, Canada and Japan) and China.

Figure 1: Growth rate of services trade over 1996-2006 for the top twenty services traders in 2006

Services exporters Services importers

Source:

World Bank, Sustaining India’s Services Revolution: Access to Foreign Markets, Domestic Reforms and International Negotiations (2004); author’s own calculations.

Considering next the composition of services trade in these two economies, computer-related (“CRS”) and other business services (“OBS”) dominated India’s sevices trade in 2010, followed by transportation and travel services (see Figure 2). In the case of the EU, the most traded services in 2011 consisted of OBS, transportation, and travel (see Figure 3).

Figure 2: India’s trade in services by main categories (2010 USD millions)

Source: UN Services Trade Database

Figure 3: Extra-EU trade in services by main categories (2011 € billions)

Source: Eurostat

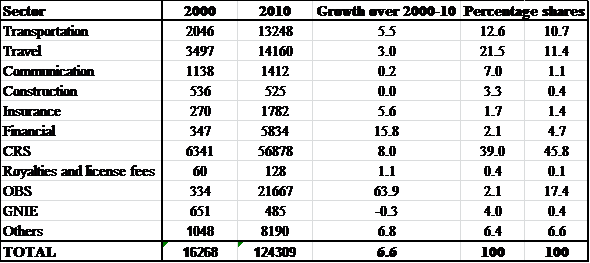

India’s services exports also changed dramatically over the last decade, both in terms of value (more than a six-fold increase from US$16.3 to US$124.3 billion) and structure (see Table 2). Significant changes in export structure occurred in the share of travel services, down from 21.5% in 2000 to 11.4% in 2010; communication services, down from 7% to 1.1%; CRS, up from 39% to 45.8%; and OBS, up from 2% to 17.4%. In terms of growth rates, OBS showed a whopping 64 times rise in services exports over 2000-2010, followed by financial services where exports grew nearly 16 times.

Table 2: Evolution of India’s Service Exports 2000, 2010 (USD mn)

Source: UN Services Trade Database; own calculations

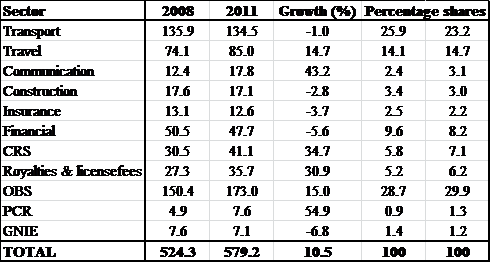

Changes in EU27 services exports, on the other hand, have not been comparable to those of India (see Table 3). In terms of value, services exports increased by 10.5% from €524.3 to €579.2 billion over 2008-2011. The structure has also remained fairly stable over time (see Table 3 below), although some sectors witnessed considerable growth in exports – personal, cultural and recreational services (“PCR”), communication services, CRS, and royalty and license fees.

Table 3: Composition of EU27 service exports 2008, 2011 (€bn)

Source: Eurostat

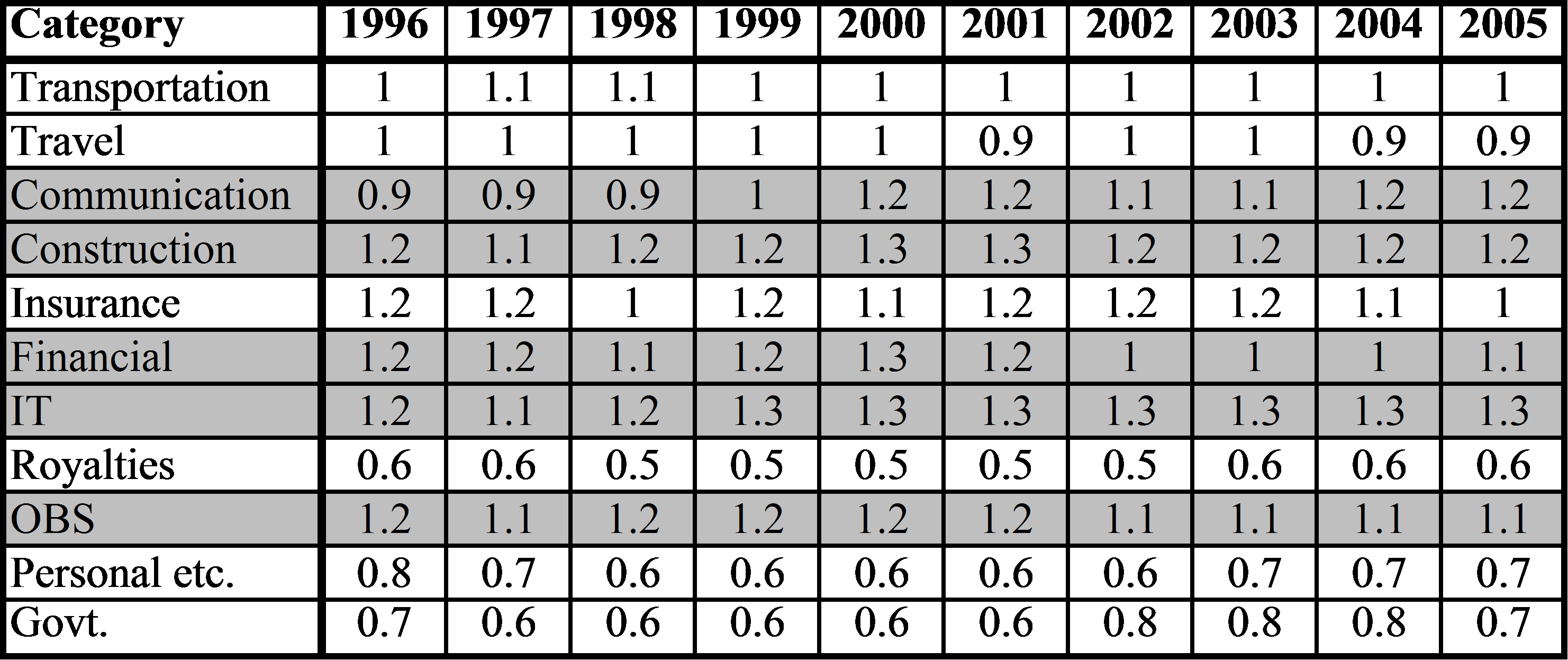

In order to compare the global competitiveness of these two economies in the export of these various services, analysts consider indices of Revealed Comparative Advantage (“RCA”) from the Commonwealth Secretariat (2009) reported in Tables 4 and 5 below. The RCA index for a given services sector in country A is calculated by taking the share of the sector’s exports in A’s total exports of services, and dividing this by the ratio of a comparator’s exports in this sector to the total services exports of the comparator. An RCA index exceeding unity indicates a comparative advantage in the sector, while a value less than one indicates a comparative disadvantage. The Report used the OCED and India as a comparator instead of the rest of the world because of data constraints – the combined services exports of the OECD and India made up more than 75% of global services exports in the last decade.

Table 4: India’s Revealed Comparative Advantage in Services

Source: Commonwealth Secretariat, Innocent Bystanders: Implications of an EU-India Free-Trade Agreement for Excluded Countries, Commonwealth Secretariat, London (Feb, 2009).

Table 5: The EU’s Revealed Comparative Advantage in Services

Source: Commonwealth Secretariat, Innocent Bystanders: Implications of an EU-India Free-Trade Agreement for Excluded Countries, Commonwealth Secretariat, London (Feb, 2009).

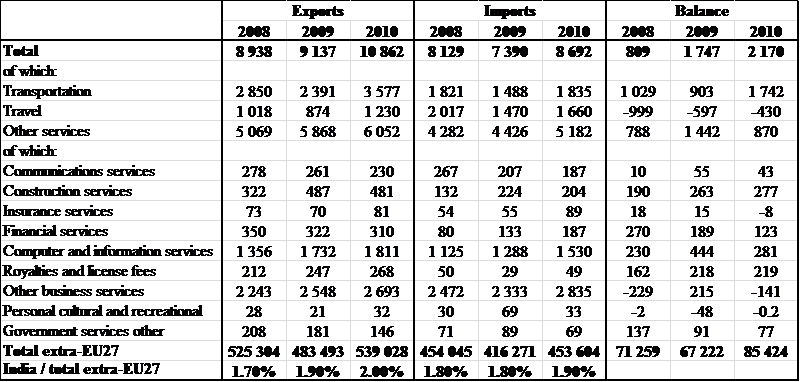

Finally, looking at EU27-India bilateral trade in services in Table 6, the reported value of this trade increased from €17 billion in 2008 to €19.6 billion in 2010. Putting things in perspective, this bilateral services trade accounted for 12 percent of India’s global services trade in 2010 but only 2% of extra-EU27 services trade. The major bilateral trading services sectors include OBS (28% of total bilateral services trade in 2010), transportation (share of 27%), CRS and travel services (together making up for 32% of total bilateral services trade), with the EU showing a surplus in most sectors except travel, OBS, and PCR services.

Table 6: EU-India Bilateral trade in Services (€ millions)

Source: Eurostat

Barriers to services trade between EU-India

Despite the importance of the services sector and its growing share in bilateral trade between these two partners, there are significant barriers to services trade between the two. According to the World Bank’s recently released services trade restrictiveness index (“STRI”), India has an overall value of 65.7 which places it amongst economies with the most restrictive policies on services trade. Most EU economies, on the other hand, are far less restrictive, overall STRI value averages around nineteen for EU-15 and around sixeteen for the “new” member states.

In general, India’s services suffer from simultaneously excessive and inadequate regulation. Many explicit and implicit restrictions – tax incentives and labour laws for instance – favour small scale units and discriminate against larger firms. Weaknesses in the institutional and regulatory regimes have resulted in disparities in the quality of services and the abilities of professionals. Legitimate universal access goals are pursued not based on the most efficient means but through elaborate restrictions involving efficiency losses without any commensurate gain in equity and access. These policies result in domestic firms that are sub-optimal in size, operate in a weakened regulatory environment, and are burdened with the legacy of pursuing equity goals. See, e.g., World Bank, Sustaining India’s Services Revolution: Access to Foreign Markets, Domestic Reforms and International Negotiations (2004).

“Imports of services to India suffer from a range of horizontal barriers such as archaic laws, multiplicity of rules and regulations, inconsistent practices across states and multiplicity of contact points at different levels of bureaucracy, regulatory gaps, public sector bias, and limits on foreign investment and ownership.” Commonwealth Secretariat, Innocent Bystanders: Implications of an EU-India Free-Trade Agreement for Excluded Countries, Commonwealth Secretariat, London (Feb, 2009). Some of these issues, such as inconsistent practices across states, different levels of bureaucracy, and restrictions on the movement of services providers, are also concerns on the part of the Indian services exporter in the EU market. India’s services sector-specific FDI policy is listed in Table 7 below

| SERVICE SECTOR | ISSUES |

| Accountancy | FDI not allowed; Foreign Services Providers (FSP) not allowed to undertake statutory audit of companies. Only partnership firms allowed with number of partners limited to 20. |

| Architecture | No cap on FDI. Foreign architects need to be registered by the Council of Architecture as individuals. Appointment of foreign architects as consultants to Indian architects subject to case-by-case approval by GoI. |

| Legal | FDI not allowed. International law firms not allowed presence. Indian advocates cannot enter into profit-sharing arrangements with non-Indian advocates. |

| Computer-related or software services | No cap on FDI. No explicit barriers on commercial presence of foreign firms. |

| Management and Consultancy | No cap on FDI. Foreign firms must be incorporated in India. |

| Postal | FDI not allowed. |

| Courier | No cap on FDI |

| Telecommunications | Up to 74% FDI allowed. |

| Audio-visual Services | No cap on FDI in motion picture. |

| Construction and related engineering | No cap on FDI. |

| Distribution | No cap on non-retail segments, 51%limit on FDI in multi-brand retail subject to state implementation, up to 100 percent FDI in single-brand retail. |

| Education | FDI permitted without cap through the automatic route. |

| Environmental | FDI permitted without cap through the automatic route. |

| Financial services (Insurance) | Foreign equity limit of 26% in most segments. Minimum capitalization norms. |

| Financial services (Banking) | Private domestic equity limited to 49% and foreign equity limited to 74% with 10% voting rights. FDI and portfolio investment in nationalized banks subject to overall statutory limits of 20%. |

| Health and Social Services | No cap on FDI. Movement of FSP subject to registration by the Medical/Dental/Nursing Council of India. |

| Tourism | No cap on FDI. |

| Recreational, Cultural and Sporting | FDI is permitted in entertainment services (including theatre, live bands and cultural services), libraries, archives and museums. Up to 74% FDI allowed in broadcasting services, 26% FDI allowed in print media. Lottery, betting and gambling are not allowed. |

| Transport | One hundred percent FDI in maritime and road transport, 49% FDI in aviation. |

Source: India’s FDI Policy (2012)

Information from the EU’s Market Access Database suggests that limitations on the operation of foreign banks and a relatively closed insurance sector continue to be issues of concern. In general, the EU has key strategic interests in the Indian market in banking, finance, insurance, retail, accountancy, legal, telecom, and maritime services. Sectors like IT and telecom are already significantly liberalized in India while others such as construction, health, banking, insurance, education, retail, and courier are moderately liberalized. Legal, accountancy and postal services, on the other hand, are completely closed. From the perspective of the BTIA, the EU would like to consolidate their market access in Indian IT and telecom services to significantly improve market access in the moderately liberalized services and to open up the closed sectors.

The WTO’s General Agreement on Trade in Services classifies four “modes” of services delivery; these are the different ways in which services can be traded across borders. Mode One is the cross-border supply of services. An illustration of this is business process outsourcing units in India doing online medical transcriptions. Mode Two is consumption of services abroad, such as Indian students going abroad to study. Mode Three is commercial presence, such as foreign banks setting up operations in India. Finally, Mode Four is the movement of natural persons across borders to deliver services, such as Indian software professionals delivering and testing a system in London. The important issues for India are market access for cross-border services (Mode One) and service professionals (Mode Four including contractual service providers and service professionals related to Mode Three) and increasingly foreign investment in services abroad (Mode Three).

The Ministry of Commerce and Industry maintains that the focus subsectors are likely to include computer and related services, financial services, and energy services. In Mode One, India would like to increase the coverage of subsectors to research and development, dental and health related sectors, and telephone-based services. In Mode Three, issues relate to the need for huge minimum capital requirements imposed by the EU, residency requirements, restrictions on legal entity, and the absence of national treatment. In Mode Four, India would like to press for the mutual recognition of qualifications to make effective market access possible.

Other issues relate to the avoidance of double taxation on social security benefits of Indian services professionals abroad; visa issues and labour market and economic need tests for Indian services providers abroad; and EU domestic regulation being more burdensome than necessary. In addition to specific modal interests, general issues of priority for India are transparency in EU policies and their implementation and the need for harmonization of EU policies across member states. “As an illustration from the financial services sector, India will argue that banking sector licenses granted by any one EU Member be acceptable across the EU as the need to apply for separate licenses in each EU Member state has been pointed to as one of the cumbersome elements of trade in banking services with the EU by Indian government officials.” Commonwealth Secretariat, Innocent Bystanders: Implications of an EU-India Free-Trade Agreement for Excluded Countries, Commonwealth Secretariat, London (Feb, 2009).

From India’s perspective, it may be easier to negotiate provisions on Modes One and Three into the BTIA and also examine regulatory issues vis-a-vis Mode Four. It may, however, be more difficult to negotiate mutual recognition agreements across services between these two trading partners. From the EU’s perspective, it may be much easier to consolidate market access in India’s liberal sectors and increase access in the moderately liberalized ones. Opening up completely closed sectors, on the other hand, is likely to be the most difficult to achieve.

Services trade is likely to be a major component of the EU-India BTIA. Both parties have a strong interest in the service sector and in mitigating the many barriers to mutual trade. The BTIA, therefore, provides a useful opportunity to both partners to address these barriers. This said, there are two notable caveats to preferential services liberalization.

First, the sequence of liberalization matters more in services trade than in the case of goods trade because location-specific sunk costs of production are important, so even temporary privileged access for an inferior supplier can translate into a long-term market advantage. Mattoo, A. & C. Fink, Regional Agreements and Trade in Services: Policy Issues, World Bank Policy Research Working Paper 2852 (June 2002). First-mover advantages for an inferior supplier would have durable adverse welfare consequences relative to a more even-handed liberalisation, and the country could be stuck permanently with weaker providers even when it subsequently liberalizes on an MFN basis. Such incumbency-advantages are likely to be particularly important in services with network externalities.

Second, it may be difficult, if not impossible, to open up some sectors on a preferential basis. While market access and national treatment restrictions may be relaxed on a preferential basis, the removal or reduction of most regulatory barriers has more or less to be on an MFN basis. For instance, the number of partners in Indian accountancy firms is restricted to twenty. If Indian regulatory authorities relaxed this rule, it would be extremely difficult to limit this regulation to preferential suppliers. Similarly, improved prudential regulation of the financial sector would be applicable to everybody, not just to the EU and Indian firms. In such cases, de jure preferential liberalization becomes de facto MFN liberalization. Sauvé, P. & A. Shingal, Reflections on the Preferential Liberalization of Services Trade,’ Journal of World Trade 45:5, (2002).

Anirudh Shingal is a Senior Research Fellow at the World Trade Institute (WTI), University of Bern; Co-leader of a Swiss National Science Foundation funded work programme on the impact assessment of trade and part of the Economics faculty on the Masters in International Law & Economics (MILE) programme at the WTI. A PhD in Economics from the University of Sussex, Anirudh specialises in International Economics, Applied Econometrics and Development.

His research on trade in services, government procurement and preferential trade agreements has been published in peer-reviewed journals as well as by the World Bank, the European Commission and the Commonwealth Secretariat. Anirudh is also affiliated with the Centre for the Analysis of Regional Integration at Sussex (CARIS) and has also worked with the World Bank, WTO and the private sector. Anirudh graduated ‘summa cum laude’ on the MILE Program at the WTI and also holds a Masters degree in Economics from the Delhi School of Economics. His undergraduate degree was in Economics (Honours) from St. Stephen’s College, Delhi University. He can be reached at anirudh.shingal@wti.org.